Ebrima Y Jallow

2 mins read

Digital payments in The Gambia have come a long way. What began with basic mobile money transfers has evolved into a diverse ecosystem of wallets, remittance platforms, payment gateways, and infrastructure providers.

By 2026, most Gambians use multiple payment platforms, one for transfers, another for bills, another for business. While this growth is positive, it has also introduced fragmentation.

This article looks at the leading payment companies in The Gambia in 2026, what each does well, and why the market is now shifting toward all-in-one payment aggregation, led by platforms like Waychit.

The Gambian Payments Landscape in 2026

Today’s payment ecosystem can broadly be grouped into three categories:

- Mobile wallets focused on peer-to-peer payments

- Wallet + remittance hybrids linking diaspora funds to local use

- Payment infrastructure and gateways enabling interoperability

Each category plays an important role — but none, on its own, fully solves payments for users, merchants, and institutions.

Leading Mobile Wallets

Wave Mobile Money

Wave is one of the most widely used mobile money platforms in The Gambia. It’s popular for person-to-person transfers and everyday payments, driven by a simple user experience and low fees.

Strength: P2P transfers, widespread usage Limitation: Single-wallet ecosystem, limited merchant and institutional workflows

AfriMoney (Africell)

Backed by Africell’s large subscriber base, AfriMoney is a massive player for transfers, airtime/data, bill payments, and merchant payments — especially for users already within the Africell network.

Strength: Telecom reach, everyday payments Limitation: Wallet-centric, limited aggregation across payment methods

QMoney Financial Services

QMoney is one of The Gambia’s earliest mobile money providers and remains relevant for transfers, merchant payments, and wallet-based services.

Strength: Early mover, stable wallet services Limitation: Less focused on advanced merchant, API, or institutional needs

Wallet & Remittance Hybrids

NAFA Financial Services

NAFA combines a digital wallet with a strong remittance payout network, helping users receive funds from abroad and use them locally.

Strength: Remittance access, hybrid digital–cash model Limitation: Payments mainly tied to remittance flows

APS Digital Wallet

APS has evolved from forex and remittance services into digital wallets, offering users another option for receiving and spending funds.

Strength: Remittance-linked payments Limitation: Narrow use cases beyond wallet transactions

Yonna Wallet

Yonna focuses on everyday payments such as airtime, bills, and school fees, contributing to broader financial inclusion.

Strength: Simplicity, local use cases Limitation: Limited merchant and institutional depth

Payment Infrastructure & Gateways

Gamswitch Company Ltd

Gamswitch is critical national infrastructure, the payment switch connecting banks, mostly, and some payment service providers. While not consumer-facing, many platforms rely on it behind the scenes.

Strength: Interoperability at the national level Limitation: Not a direct solution for merchants or consumers

The Gap: Fragmentation Everywhere

Despite having many payment companies, a clear problem remains:

- Users juggle multiple wallets

- Merchants integrate several payment methods separately

- Institutions struggle with disbursements, controls, and reporting

- Settlements and reconciliation remain manual and inefficient

The ecosystem has plenty of tools — but no unifying layer.

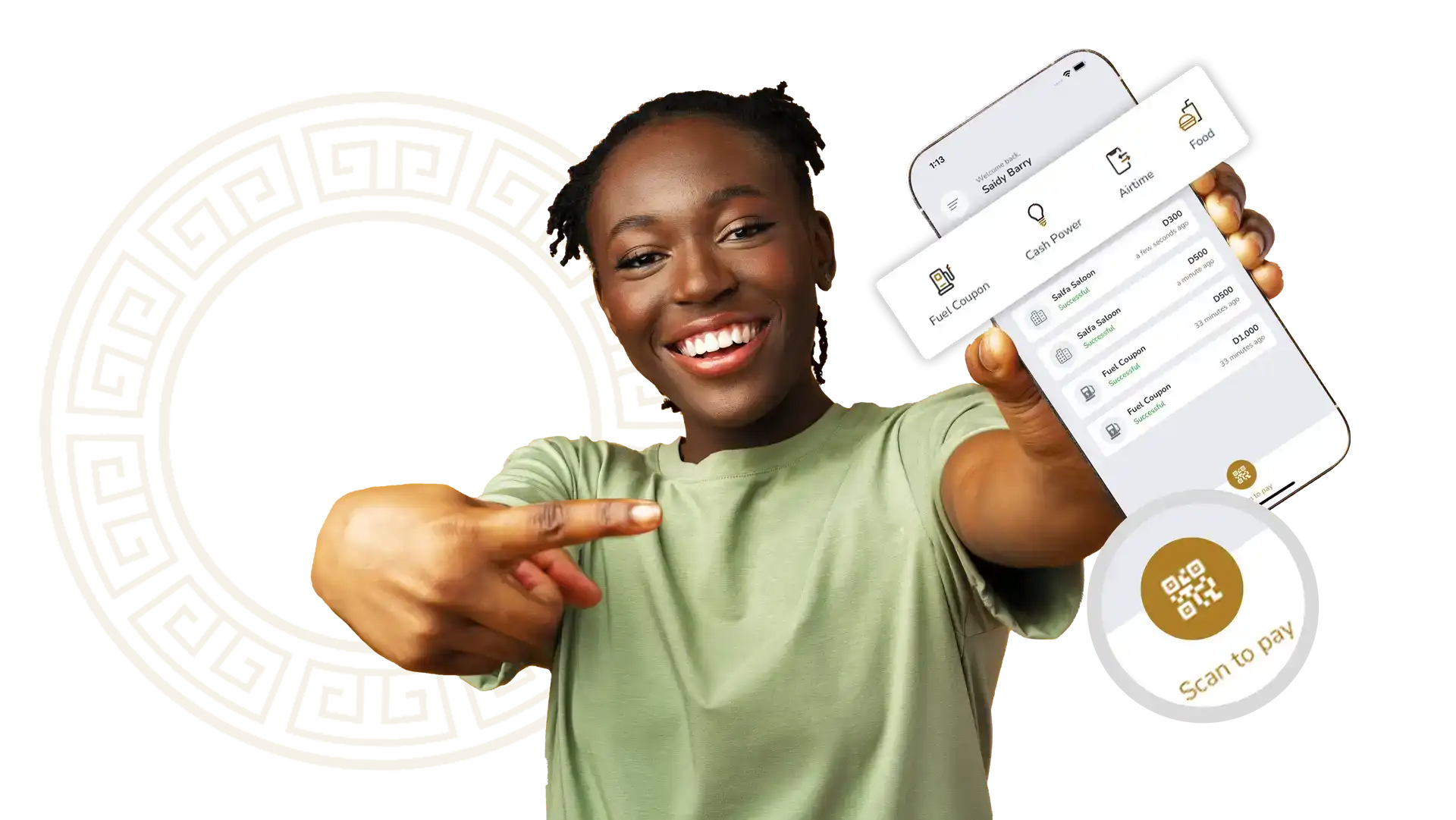

Waychit — The All-in-One Payment Layer for The Gambia

This is where Waychit stands apart.

Waychit is not another wallet. Instead, it functions as a payment aggregator and orchestration layer that sits above wallets, banks, and cards, connecting them into one seamless system.

What makes Waychit different

- Supports all major mobile wallets in The Gambia

- Integrates banks and cards (Visa & Mastercard)

- Allows users to pay with any linked payment method

- Merchants receive instant settlement directly into their bank accounts

- No locked balances or closed ecosystems

Built for real-world use cases

Waychit goes beyond transfers by powering:

- Fuel payments & institutional fuel allocation

- Food vouchers for staff and organizations

- Utilities (internet, power, bills)

- Airtime & data (single and bulk)

- Merchant payments, invoicing, and POS

- APIs for apps, websites, and enterprises

Waychit connects users, merchants, institutions, and developers, all on one platform.

Why the Market Is Moving Toward Aggregation

In 2026, leadership in payments is no longer about owning a single wallet. It’s about:

- Interoperability

- Instant settlement

- Enterprise and institutional readiness

- One integration instead of many

This shift naturally favors platforms that connect the ecosystem, rather than compete inside silos.

Final Thoughts

The Gambian payment ecosystem is richer than ever — but also more fragmented. Mobile wallets, remittance platforms, and infrastructure providers each solve part of the problem.

Waychit solves the whole workflow.

By acting as a neutral, all-in-one payment layer, Waychit represents the next phase of digital payments in The Gambia, where users pay how they want, merchants settle instantly, and institutions operate at scale.

In 2026, that’s what leadership in payments looks like.

Payments

Fintech

Gambia